Banking News Roundup – Week of October 21

Open banking, earnings, index funds, California's nonbank registry, CRE's "extend-and-pretend" problem, bank runs, and M&A, in a five minute read.

Open Banking

The Consumer Financial Protection Bureau (CFPB) released its final “open banking” rule, which will apply to banks and credit unions with $850 million or more in assets, credit card issuers, and “data providers” (a term to be further defined in future rulemaking). The rule’s scope is vast and complex, and it will be phased in through April 1, 2030. According to the CFPB, the new framework will usher in an era of better pricing and products while enhancing consumer privacy. Critics, however, argue that the rule is a threat to data security, and opens the door for unregulated entities to potentially misuse customer information.

In response, the Bank Policy Institute (BPI), the Kentucky Bankers Association, and Forcht Bank, N.A., filed a lawsuit the day after the rule’s release, arguing that the CFPB exceeded its mandate under Section 1033 of the Dodd-Frank Act. They claim the rule, intended to grant consumers access to their data, unlawfully extends access to third-party service providers and leaves banks vulnerable to litigation.

Earnings

Earnings season was in full swing this week, with many regional and smaller banks reporting. Some common themes emerged. Ally Bank was bogged down by rising auto loan defaults, mainly from post-pandemic lending in 2022, while Capital One was seemingly unaffected by the troubled vintage. Commercial & industrial (C&I) loan growth was slow for Regions, but not at Dime, which is handily capitalizing on Signature Bank’s demise. First Citizens revised its forecasts downward, citing slow loan growth at its Silicon Valley Bank (SVB) subsidiary amid a contraction in startup funding. Provision for loan losses has increased for banks with large commercial real estate (CRE) portfolios, with Flagstar posting a whopping $242 million provision expense as it addresses issues in New York Community Bank’s (NYCB) legacy portfolio. Bank stocks took a hit at the close of the week, led by Flagstar with an 8.3% drop, followed by smaller declines for JPMorgan and Goldman Sachs.

Regulation

Bloomberg reports that the Federal Deposit Insurance Corporation (FDIC) has requested information from BlackRock and Vanguard regarding their bank investments and specifically seeking proof that they remain passive shareholders. This struck some people as odd, since the FDIC’s public comment period on the proposed rule remains open until November 18, with no final rule issued yet. BlackRock, echoing concerns from the U.S. Chamber of Commerce and others, called on the FDIC to withdraw the proposed rule.

California launched its registry for nonbank financial services providers. Debt settlement, earned wage, secondary education financing, and student debt relief firms must register by February 15, 2025. California’s Department of Financial Protection and Innovation (DFPI) will collect information from registered firms over the next four years and submit its findings to the state legislature, which will then determine if the registration requirement will continue.

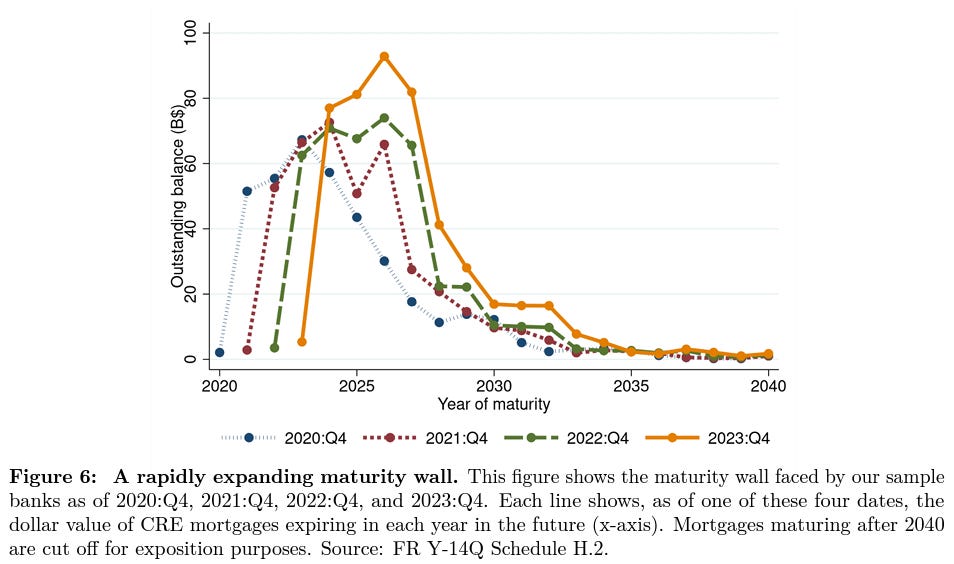

CRE

The Federal Reserve Bank of New York published a report titled , Extend-and-Pretend in the U.S. CRE Market, which analyzes the impact of extending loan maturities and warns of a looming “maturity wall” in the CRE market.

Tracy Alloway of Bloomberg’s Odd Lots points out that banks can deal with the maturity wall by just continuing to extend. That said, the amounts in question are nothing to sneeze at, especially when loans coming due within the next three years represented 27% of marked-to-market bank capital as of the fourth quarter of 2023.

Wells Fargo warned that it may lose $2 billion to $3 billion on its CRE office loan portfolio. While the bank has reserved for these potential losses, the announcement added to the broader market pessimism regarding office loans.

Bank Runs

The Financial Stability Board (FSB) released a report on the March 2023 bank failures, titled Depositor Behaviour and Interest Rate and Liquidity Risks in the Financial System: Lessons from the March 2023 banking turmoil. The report finds that a “weak tail” of banks remains vulnerable to solvency and liquidity risks. It also highlights that life insurers and nonbank real estate investment firms may face similar risks. Additionally, the FSB examined the role of social media in exacerbating bank runs, noting its potential influence in the cases of SVB and Credit Suisse.

To mitigate future high-speed bank runs, the report recommends developing metrics to monitor deposit vulnerabilities, especially uninsured deposits and concentrations, and suggests enhanced social media monitoring and greater emphasis on crisis communication capabilities in resolution planning. Although the United States has existing social media guidance from 2013, its approach is relatively limited.

M&A

Virginias’s Atlantic Union Bankshares inked a deal to acquire Maryland-based Sandy Spring Bancorp in a $1.6 billion all-stock transaction. Atlantic Union will raise $336 million to finance the transaction via a common stock offering and plans to sell approximately $2 billion of Sandy Springs CRE loans after the transaction closes. The combined institution will have total assets of $39.2 billion.

Tennessee’s Y-12 Federal Credit Union plans to acquire First State Bank of the Southeast in Kentucky, forming an approximately $2.4 billion entity. Hawaii State FCU, a $2.4 billion credit union, announced a merger with HMSA Employees’ Federal Credit Union, which is expected to add $50-60 million in assets. In Texas, Austin Bancorp, Inc. announced it will acquire The Chasewood Bank, creating a combined entity with $2.9 billion in assets. Terms were not disclosed for any of the transactions.